149 hectare Khi Solar One in Northern Cape. The Northern Cape is prime real estate for wind and solar, but the grid simply cannot accommodate more connections until substantial investments are undertaken by Eskom. The Western and Eastern Cape are likely to face similar restrictions.

SOUTH AFRICA’S ENERGY CRISIS IS set to proceed as usual, with Eskom’s recent announcement of another round of high-intensity stage four load shedding due to the exhaustion of its diesel budget. At the same time, the 27th United Nations Climate Change Conference (COP27) has also concluded on the note of “business as usual”, delivering a shameful and depressing outcome in a year of biblical floods, heatwaves, droughts, and other climate disasters. For South Africa, COP27 has seen the government enthusiastically agreeing to loans that will cement our path towards tepid, neoliberal energy reform, and the Potemkin village that is our “just transition”.

In this context, the debates around Eskom, our energy crisis, and the just transition will remain a mainstay of the national discourse for the foreseeable future. Of course, this means that we will also see the same myths and misconceptions repeated in the media, in political discussions, and in the statements of the fearless free-marketeers returning from their finance-finding expedition abroad.

This article will try to address some of these misconceptions, building on the research done by organisations such as the Alternative Information & Development Centre (AIDC), Naledi, the Institute for Economic Justice, Trade Unions for Energy Democracy and many others.

Myth: Regulation and bureaucratic red tape are the biggest factors holding back the rollout of renewables on a mass scale

The claim: South Africa is blessed with an abundance of excellent locations for wind and solar power generation, and the private sector is eager and more than ready to invest. Issues around energy storage and variability can be overcome – the main obstacle is the fact that independent power producers (IPPs) are not allowed to invest and build as they please.

Our response: There are a number of key issues in this myth, but the biggest is that the South African transmission grid has become a major bottleneck for new energy projects. The Northern Cape is prime real estate for wind and solar, but the grid simply cannot accommodate more connections until substantial investments are undertaken by Eskom. The Western and Eastern Cape are likely to face similar restrictions.

Eskom’s Transmission Development Plan predicts that this issue will not be fully resolved in the next decade, due to constraints in procurement, the difficulty of obtaining agreements with landowners (servitudes), and finances. This upgrading will require at least R47.8bn in capital expenditure over the next five years – a difficult prospect for Eskom’s balance sheet.

At least one reason for this is historical: the country’s energy generation and consumption is situated in the coal and industrial heartlands of Mpumalanga and Gauteng, home to the coal-fed Minerals Energy Complex. The provinces with the best potential for renewables are elsewhere; they have also been those with the least energy consumption and generation capacity in the past. The configuration of our electricity infrastructure will need to be completely turned around. This is no small task for a utility that is itself undergoing a confused and difficult reconfiguration through unbundling. It is certainly not one that the private sector would be eager to take on.

Myth: A healthy dose of competition is needed for Eskom to get its house in order

The claim: One of the best cures for Eskom’s evident inefficiencies and mismanagement is to loosen its monopoly on the energy sector and place it in competition with lean and efficient IPPs. This will force the utility to kick itself into gear, trim the fat, and discipline itself – or else face a firm slap from the free hand of the new energy market.

Our response: Eskom’s problems go far deeper than this often-repeated claim from the business press would suggest – usually one made in the context of Eskom’s financial position or labour conflicts. Firstly, we ought to be clear that it is specifically Eskom Generation that would be put in competition with the private sector, should unbundling and marketisation proceed as planned.

Eskom Generation would enter this competition on a very poor footing. It would likely be handed the brunt of Eskom’s debt (especially the odious World Bank loans for Medupi and Kusile), as well as the task of running the expensive, ageing fleet of coal-fired power stations, alongside the costly task of decommissioning the oldest ones. So it would have to catch up with overwhelming maintenance issues, and facing up to steadily increasing coal prices. While it has the advantage of providing the overwhelming majority of our baseload power requirements, as more private generation comes online, non-labour-intensive renewable IPPs will begin to eat into its market share, decreasing its revenues.

The Sam Tambani Research Institute has done research on energy sector unbundling in Africa. It has found that it leads to either minor or negative gains in efficiency for power utilities, while leading to massive job losses of up to 38%, as well as higher energy costs. The minor increases in efficiency and productivity from the “corporate austerity” faced by future Eskom Generation are far from a cure for the utility’s financial woes, while the consequences of its profit maximisation drive will be keenly felt by the working class of the country.

Myth: The move to clean energy is inevitable and imminent as renewables are the cheapest form of generating electricity

The Claim: The main forms of generating renewable energy – namely wind and solar – have the cheapest “levelised cost of electricity” (LCOE, the R/Kilowatt) of any energy generating source, including coal or nuclear. The transition to clean energy therefore does not even require a particularly strong political push; it will occur through the laws of economics.

Our coal-fired power stations and related industries spew a host of toxic emissions, poisoning both the soil and the people reliant on them. In Mpumalanga, the Kriel power station is the second largest point source of sulphur dioxide emissions in the world.

Our Response: The LCOE of renewables has begun to be fully competitive with fossil fuel sources such as gas and coal in recent years, but this obscures part of the picture. For one, the low cost of generating renewable energy has in part been protected by extensive public subsidies, protections, or feed-in tariffs introduced in almost all countries with currently growing private renewable sectors. Secondly, the low LCOE does not take into account the system costs of integrating renewables into the grid, such as the very costly battery storage and grid capacity upgrades required. Thirdly, we are globally not actually seeing yet an energy transition; only an energy expansion.

Renewables account for around 80% of new capacity added, but this rate of growth is still not enough to break from fossil fuels, which account for around 90% of all capacity globally. There is a rise in demand for all energy types globally, and renewable power must both expand as much as it can to supplant existing fossil fuel generation, as well as outpace new additions. None of this means that renewable power is a dead end; it simply calls into question the argument that a market-led energy transition will come about due to simple economic factors.

Myth: South Africans can look forward to lower electricity prices as a result of coming energy sector reforms

The Claim: For most of us, the price of electricity is already hard enough to stomach even without Eskom’s requested 32% tariff increase. However, with unbundling and the entry of renewable IPPs into the market, competition will drive prices down, as Eskom loses its monopoly.

Our Response: Although it may be difficult to believe, the fact is that Eskom is actually charging tariffs that are below an adequate rate of return for the utility, given its immense cost pressures. Given the steadily increasing price of coal, diesel, and gas, truly “cost-reflective” tariffs are likely to continue increasing. And given the fact that Eskom’s baseload power will be required for more than the next decade at least, the benefits of cheaper renewable IPPs will not translate into consistently cheaper tariffs. Finally, the energy sector reforms, such as changes to the Electricity Pricing Policy, are set on allowing for Transmission to “pass-through” the costs of the intensive grid upgrades and balancing work that will be required to the end user; in other words, the work of overhauling our energy sector will be financed by what we all put into our pre-paid meters.

Myth: The explosive growth of the local renewable energy sector will absorb job losses as coal is phased out, allowing for a “‘just transition

The Claim: While not all fossil-fuel jobs can be replaced, South Africa is well situated for the growth of a strong, renewables-driven, green industrialisation programme. This may be whether through manufacturing solar panels and wind turbines or through the creation of new regional value chains in batteries or green hydrogen – a process well supported by the Just Transition Investment Plan.

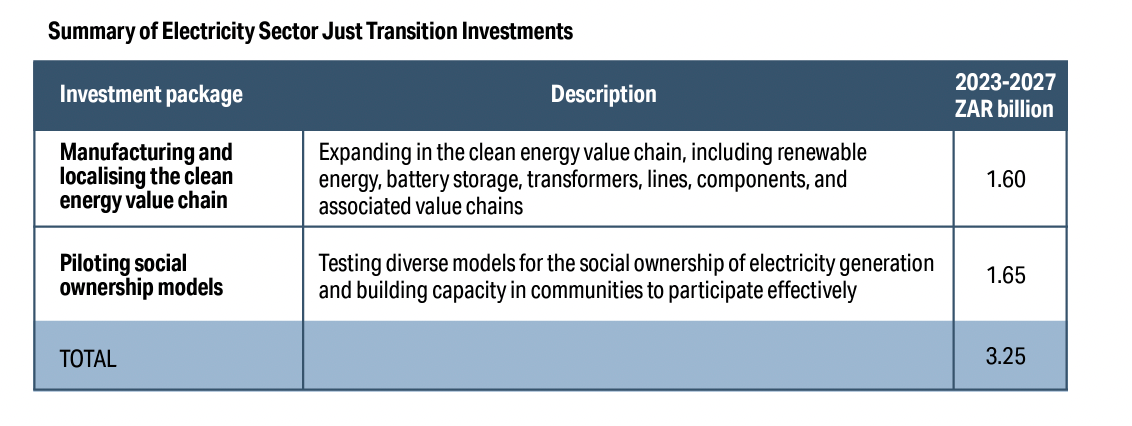

Our Response: Green industrialisation is a process that would require not only significant investment in these industries but also protection from the (up to 50% cheaper) foreign imports that have kept the local RE industry trimmed down to a single solar PV manufacturer. This is especially true should it take place on the scale required to replace the well over 100,000 jobs in the coal and related industries. Unfortunately, the Just Transition Investment Plan – despite the overtures made towards local green industrialisation – allocates a measly R1.6bn to the localisation of RE value chains.

There is little to be found in the way of protection either. In fact, the government is looking at relaxing local content requirements for REI4P projects due to their already-low profit margins and consequent inability to reach financial close. IPPs – especially those owned by foreign TNCs – have already been accused of bypassing local content requirements, bringing their own specialists and parts from abroad, while leaving South Africans largely with temporary construction jobs. In the absence of serious subsidies and import tariffs – as was common sense in the good old days of import substitution industrialisation – there is little reason to have any faith that these green jobs will materialise.

Myth: South Africa only emits around 1% of global greenhouse gas (GHG) emissions, so we should not be concerned with rapid decarbonisation

The Claim: South Africa might be the 11th biggest emitter, but this is misleading. Countries such as China, the United States, India and Russia together produce the vast majority of all emissions, while we account for only 1%. It is therefore nonsensical to call for urgent decarbonisation in South Africa, at the cost of worsening our socioeconomic crises.

Our Response: It may be true that we are responsible for only a small percentage of total GHG emissions, but we are about equal with China when it comes to GHG emissions per person. Percentages of GHGs are also not the only reason to decarbonise. For one, our coal-fired power stations and related industries spew a host of toxic emissions, poisoning both the soil and the people reliant on them in places such as eMalahleni and the Vaal Triangle. In Mpumalanga, the Kriel power station is the second largest point source of sulphur dioxide emissions in the world. A short hike away is Sasol’s Secunda coal-squeezing complex – built for the fuel security of the apartheid regime and today the single biggest point source of GHG emissions in the world.

These highly concentrated toxic hotspots ought to be closed and replaced even if they were not contributing to global heating. Secondly, we may be faced with serious economic consequences for not decarbonising. Countries in the Global North are considering a variety of taxes and border tariffs based on the carbon intensity of imports. Even electric vehicles produced locally will be covered, so using coal-powered factories and transport on petrol and diesel-guzzling trains and trucks will attract tariffs. If these carbon border tariffs are implemented in our current circumstances, our export-based industries will be devastated.

Myth: Relaxing limitations on generators for use at particular workplaces (embedded generators) is a win-win as this will allow us to decarbonise our economy while big companies foot the bill

The Claim: While waiting for unbundling, the relaxation of the licensing threshold for generators to 100MW – and potentially altogether – is a great way to begin decarbonising and getting extra capacity online at the expense of the private sector. At present, up to 80 projects have been initiated, totalling a potential capacity of 6000MW. These have been largely in the mining sector, with companies such as Anglo-American and Exxaro pushing ahead with solar installations at their mining and processing sites. This kind of power generation that is largely for own use is called “embedded generation”. These embedded generators can enter into power purchase agreements with other energy users on the grid, getting Eskom to “wheel” the electricity to the end user for a fee (in reality this is a grid balancing act, not a straight sale of electrons from one place to another).

Our Response: It is true that the relaxation of the licensing requirement will lead to the building of new renewable energy capacity. However, the question is whether this is really a win-win for everyone. While it could alleviate the pressure on Eskom in the short term, allowing for an end to load-shedding and space for Eskom to perform its maintenance, it also means that Eskom will be losing its market share – likely permanently. Moreover, those companies able to move to their own generation are going to be the wealthiest and therefore the ones most able to pay for increased tariffs. This threatens any potential pro-poor-cross-subsidisation policies for electricity tariffs.

Further, while these embedded generators will be largely renewable, and while the reduction in emissions is certainly something to be applauded, the situation gets more complex when we introduce the issue of carbon border adjustment taxes. If these are widely implemented, then the rise of embedded generation could mean a situation where the biggest and wealthiest corporations will essentially monopolise export-based industry. Local industries do not have the capital to build embedded generation. They will continue instead to be reliant on Eskom’s coal-fired power, and consequently, face higher border taxes than their bigger competitors.